Black Swan FX Trade

Recently, the Oil Market has experienced a Black Swan Moment: collapsing demand, contango issues, storage scarcity, technical forced sellers, ETF dislocation ($USO)…

All of this translated into this infamous move with negative pricess.

To be perfectly clear, it was mainly driven by technical factors on contract expiring and forced sellers as storage was full.

Future contracts for the next 6 months are now oscillating between $20 and $30. Looking at the Chart above those are prices not experienced for 3 months or more since the 80’s and 90’s.

Again, the reason is clear: the collapse of Oil Demand by 30% due to the coronavirus lockdown.

Now I would like to move to another chart:

That is a nice stable line with only some minor moves in 2008-2009 (less than 2.5%) and a bit of hiccup in 2015-2016.

What is this chart? That is the U.S. Dollar to the Saudi Arabian Riyal Chart.

Since June 1986, the riyal has been pegged at 3.75 SAR to one USD. This peg has been in place for almost 35 years like for six other countries currencies in the region. That is for the Gulf Cooperation Council with Bahrain, Kuwait, Qatar, Oman , Saudi Arabia and the United Arab Emirates.

Those dollar pegs in the Gulf Region have been very helpful for bringing stability and encouraging business.

In 2007-2008, the SAR rose to 3.70 after the Fed cut interest rates. More recently in 2015-2016, it rose when the oil market collapsed. But over time, those pegs have been holding very well and the different local governments have been very successful in maintaining them.

But now the whole region is facing an unprecedented collapsing oil market.

As ING was recently citing (https://think.ing.com/articles/gcc-currency-pegs-unprecedented-times-unprecedented-measures/), 63% of Saudi Arabia government revenues come from Oil. That number goes up to 76% for Oman.

Let’s go through different charts/data that might help understanding why those pegs in the region are at risk.

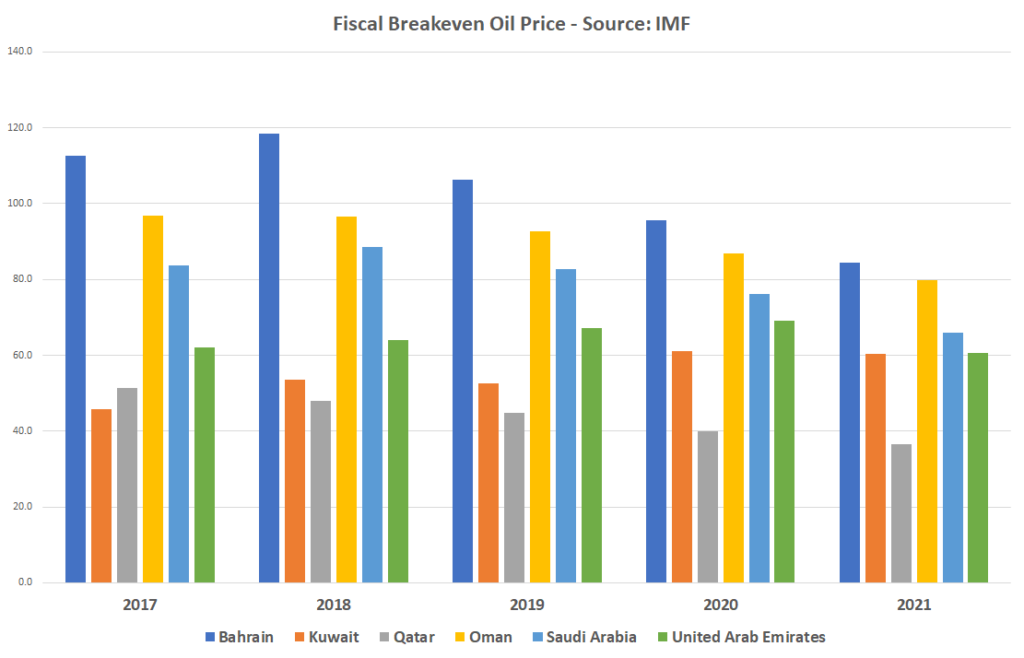

Above is the Fiscal Breakeven Oil Price by country. Only Qatar is around $40 when Saudi Arabia in 2020 is at $76 or Oman at $87. That is against WTI trading for the year 2020 in the $20-$30.

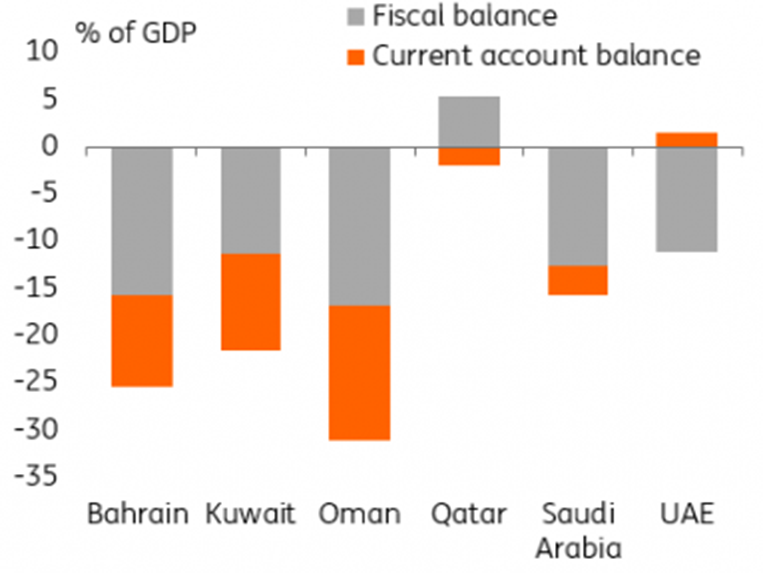

That translates into the following chart from ING:

The country most at risk in the region is Oman which is running very high dual and unsustainable deficits.

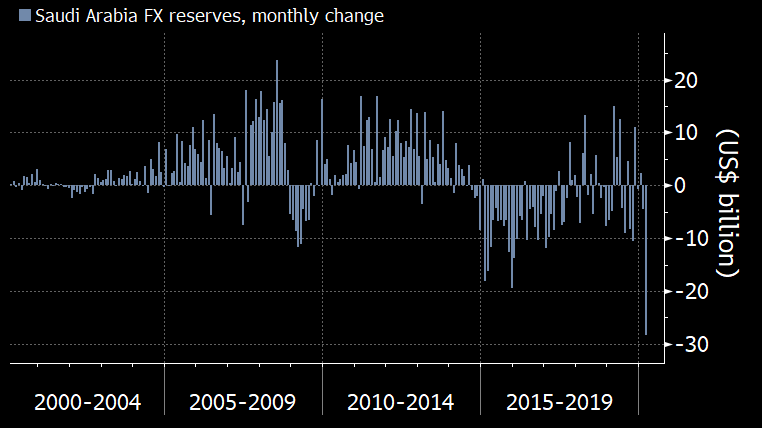

Above is the chart of Saudi Arabia Foreign Exchange Reserves for the last 10 years. As you can see since the peak in 2015, the trend has been deteriorating. That goes hand in hand with Oil coming down.

In March only, Saudi Arabia reserves collapsed by $27 billion. Since then, Oil has been coming down massively and Saudi Arabia is facing even more pressure on its revenues as output will be cut.

Source: Javier Blas – Bloomberg.

Against all those negative headlines, governments are trying to calm the markets by repeating their commitments in their respective pegs and their abilities to defend them.

Recently, the Saudi Finance Minister was on the tape saying:

If Oil stays here for too long, clearly the whole Region is financially at risk. It is clear that the odds of a V Shape recovery are now very low. The Oil market is facing anyhow a long and painful destocking. If we had months of over supply where we had at least 2-3 months with 20-30% imbalance and slow economic recovery, it will take time for the market to rebalance.

All of this goes against a region that already faced a shock in 2015-2016, the rising competition of U.S. production and budgets between $60 and $80.

What is the Black Swan Fx Trade?

No need to make a bad joke here but the white swan looks now as black oiled swan.

If you are a local resident in those regions, I am afraid to say it does not make sense to hold the local currencies. Even if the risk is low or might appear as very low, the pegs would be in the next 18 months under massive pressure.

One of my Saudi mentees recently told me: “SAR is linked to USD and fixed. USD/SAR = 3.75. Since I was born.”

Do you start to “smell the trade” here?

When something has been around for so many years, almost 35 years here, no one is really expecting here. And for good reasons as the regional governments have been very successful in keeping the peg.

But now think about the risk reward even with very low odds: no one is expecting those pegs to go, volatility as been very low meaning that the cost to build this trade is very low.

Clearly the problem is how to structure the trade. First again if you are a local and you hold local currencies, I would advice to put most of it in U.S. dollars.

Secondly, if you can trade long USD/SAR, you have a great risk reward with little downside and possible great upside if the peg is going.

The best trade if possible would be a call option probably with 12-18 months maturity. Those trades would have to be OTC (Over The Counter) and unless you are a hedge fund with good access to a bank FX desk that would be hard to put in place. I know that local FX dealers when asked by one of my mentees answered something along the lines of: “Are you crazy? It is never gone happen. So why should someone price this?”.

Here you could be facing execution implementation but in terms of risk reward I find this trade extremely attractive.

For those of you still not convinced, look again at what happened when in January 2015 the Swiss National Bank (SNB) decided to no longer hold the Swiss France at a fixed exchange rate with the euro at 1.20. I remember very well this Thursday morning when I was sitting to FX Traders caught the wrong way. Forget about putting a stop at 1.1990 or something, it took 2 hours for the big banks to get the fills and it was below 1.00.

I hope it helps,

Gregoire

P.S.: I covered this idea in a recent webinar. From 22:00 onwards.

Sub Section Title Here

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum.

THIS POST

LEARN ONLINE TRADING TODAY. THE PROFESSIONAL WAY.

Let us solve the problem and confusion around trading and finance management, the right way.

ACCESS FREE LECTURESUBSCRIBE

TO OUR BLOG

To receive opinions, market research, and data analysis in the Financial Markets

ABOUT

DUPONT TRADING

As a Professional Trader/Portfolio Manager/Hedge Fund Manager for almost 20 years, I know that learning how to Trade/Invest is a non-ending learning curve. This adventure is extremely exciting but needs to be ridden carefully.

In January 2018 after receiving many requests, I decided to start my own mentoring activities.

In October 2019, I launched the 4×4 Video Series to help Investors profitably manage their portfolios. By sharing my ideas/experiences and offering education through the 4×4 Video Series, I hope I can help you becoming a better investor.

Students

Testimonials

M. (Singapore)

LEARN ONLINE TRADING TODAY. THE PROFESSIONAL WAY.

Let us solve the problem and confusion around trading and finance management, the right way.

Reader Interactions