Cruel Oil

-30% in less than 2 months… after the 2014-2016 oil rout, that brings back painful memories for the sector.

In 2018, Oil has been making the headlines from Trump pushing for lower prices, to Iran sanctions, or Saudi Arabia, or OPEC…

All eyes are now on the OPEC Meeting in Vienna on the 6th of December 2018.

Are they still credible? Would they cut production? And if they do, by how much?

As headlines, comments, tweets… reverse almost every day on Oil, I just wanted to get a better picture on what is happening.

As always, charts are always very helpful.

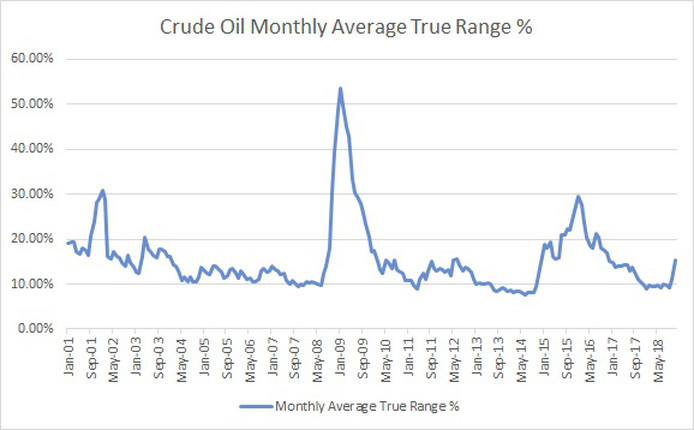

Let’s look first at the Monthly Average True Range to gauge this recent move:

Is it the start of a bigger move?

We are still far from 2015-2016 move and miles away from what happened 10 years ago when Oil was late to move when it came down, it crashed. 2007-2009 faced a demand shock, whereas 2014-2016 was more about a “positive oil supply shock”.

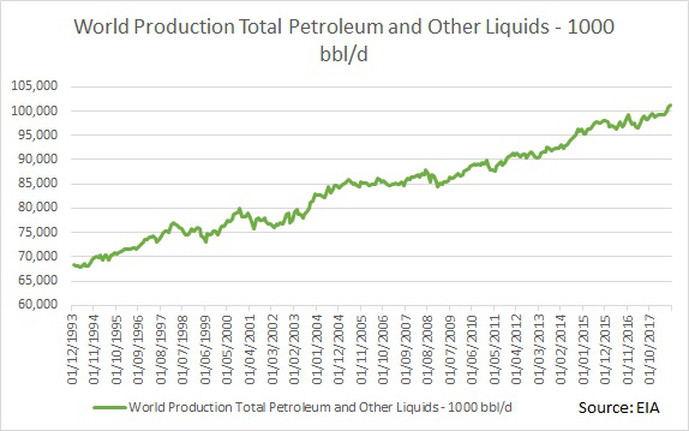

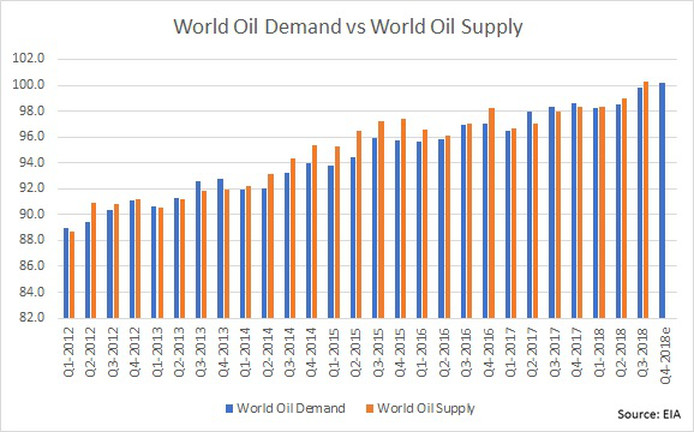

Let’s now have a look at Oil Supply:

Steady it goes, year after year.

Despite many warnings (that started decades ago!!!) from oil producers or oil majors that we will be soon running out of oil reserves soon, there is still Petroleum and Production goes up.

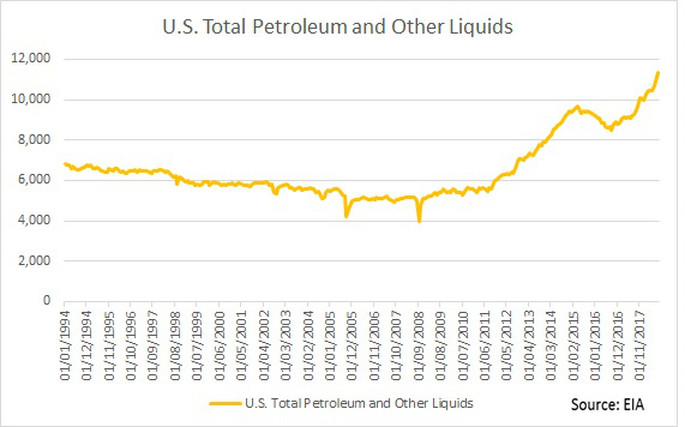

What about U.S. production recently?

The 1rst graph (U.S. Total Petroleum and Other Liquids) shows a massive ramp up with almost 2m barrels more over the last 12 months for the U.S. only.

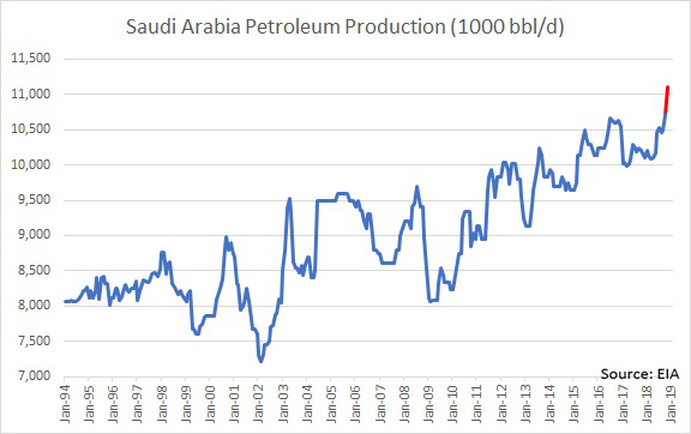

What about Saudi Arabia production?

Same here with a massive recent ramp up from 10.5m barrels per day in September to 11.1-11.3m expected in November (change in red in the above graph) and 1m barrels increase over the last 12 months.

Here we are talking of an increase of roughly 3m barrels for the U.S. and Saudi Arabia combined in the last 12 months. Yes, 3 millions!

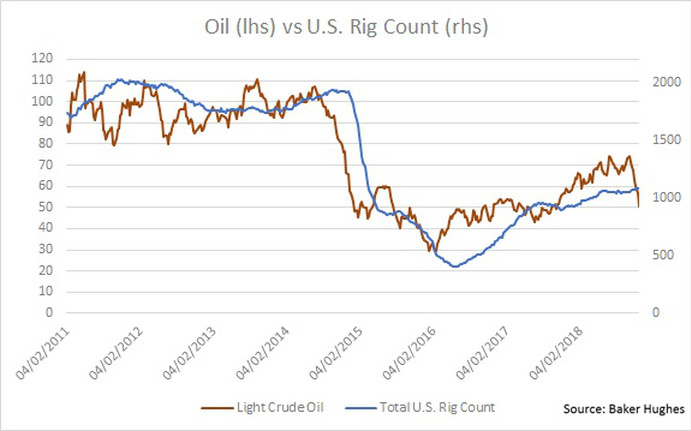

With oil stabilizing and staying above 50, more and more U.S. drillers were activating idle rigs.

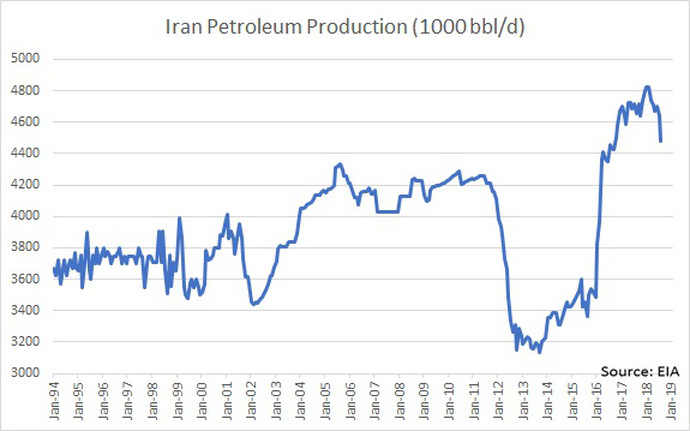

One of the narratives for higher oil was that Iran sanctions would drastically create an imbalance. So other OPEC members had to increase their productions to keep a balanced market.

So far, Iran’s oil exports have been reduced by 800k-1m barrels per day and estimations are between 1m to 1.5m when the sanctions really kick in.

If we will only take the increase from the U.S. / Saudi Arabia vs the Iran decrease, we will end up with roughly 2m surplus in 2018:

(+ 2m U.S. + 1m Saudi Arabia ) vs -1m to -1.5m Iran => surplus of at least 1.5m

I agree there are some shortcuts here but you have the big picture. Without any increase from any other OPEC member (like Russia), you have already a production increase of at least 1.5m barrels yoy.

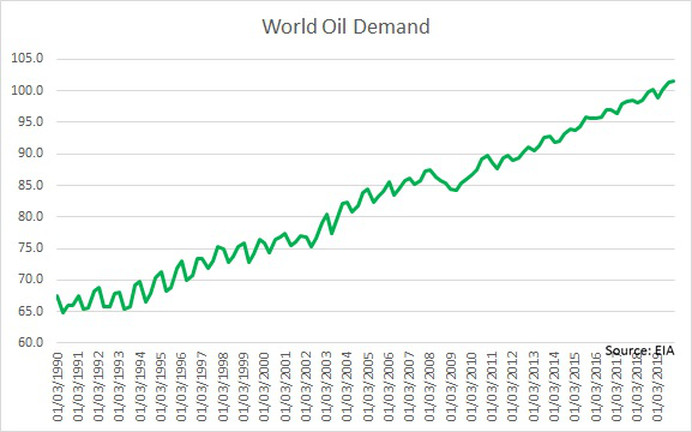

What about the Oil Demand?

IEA roughly expects 1.5-2m more barrels demand in 2018 vs 2017:

100.2m in December 2018 vs 98.6m in December 2017.

Oil Supply-Demand since 2012 = 12.6m excess.

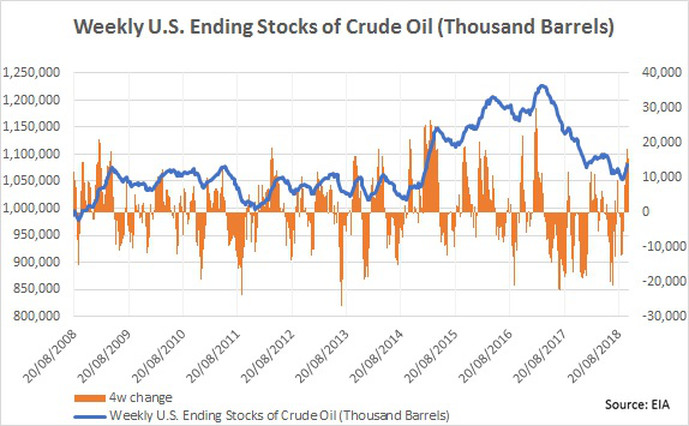

Graph for the U.S. Stocks confirming that 2017 saw a deficit:

On the demand side, 2018 should roughly see 1.5-2m more barrels.

Therefore, the production increases from the U.S. and Saudi Arabia (roughly 3m yoy) are enough to balance the combination of world demand increase (1.5m to 2m) and Iran cuts (1m to 1.5m). Oil market is correctly supplied, with a small excess of roughly 500k barrels for each of the last 2 quarters.

But clearly, recent production increases are creating more excess.

The market deficit experienced from Q2 2017 to Q4 2017 (with overall -1.6m deficit) ended up early 2018.

On that basis, assuming that the oil market was balanced in early 2018 and looking at those demand-supply numbers, it is fair to say that oil should be at the same levels or a bit below. In December 2017, crude oil was trading between $55-60.

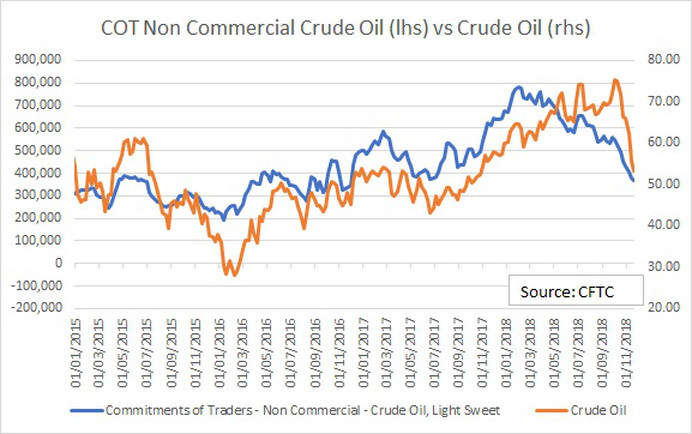

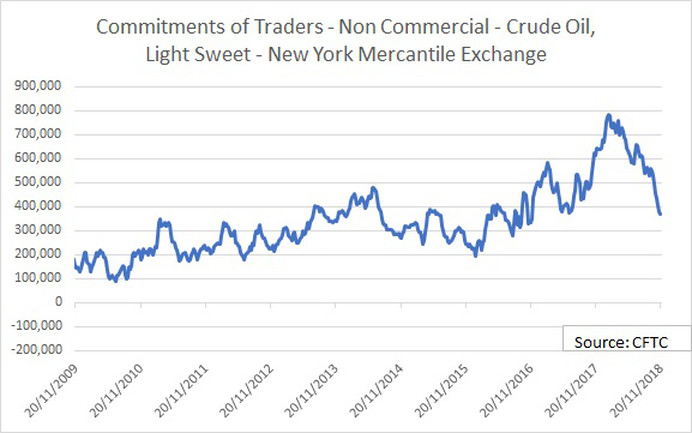

What about the market positioning?

From the Commitment of Traders report, Non Commercial Participants were aggressively long Crude oil at the start of 2018. Maximum positioning was recorded at the end of January 2018 after 12-18 months of increasing long positions.

Same graph since 2009:

Non Commercial were very, very long. The unwinding of those extreme long positions (cf. recent move vs Nat Gas) was another factor in the recent move.

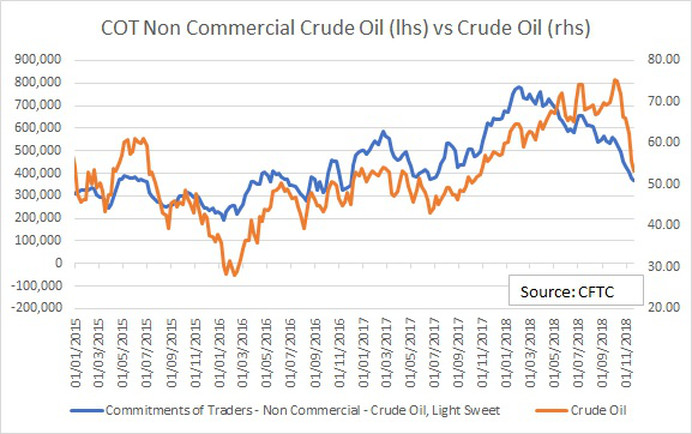

This is the recent correlation:

What about 2019?

With around 1m barrels in excess for the 1rst 9months of 2018 and with Saudi Arabia still increasing production, we could see an excess production of 1.5m to 2m.

Any cut from OPEC will need to be of at least 1.5m for a market equilibrium.

Let’s quickly look at history on the demand side:

During 2007-2009, Oil demand experienced a maximum drawdown of 3.2m barrels. I like to take 2007-2009 numbers to gauge what could happen when everything went very wrong.

Other down years were 1992 and 2012 with less than 0.6% decrease.

On average, world oil demand is up 1.5% per year since 1990.

Looking at the last 30 years Oil demand trend, the actual 1.5m yearly “excess production” could be absorbed by the end of 2019 => 1.5% of roughly 100m barrels.

But any slowdown means probably a small increase or even a decrease.

You could be talking of a delta between -3m barrels to +1.5m or 4.5m when the market is already in excess of 1.5m.

That is to say that a quick equilibrium (6-12months) for the oil market assumes:

- No big economic slowdown and steady demand growth, at least same as before.

- Oil production would stay at current levels, with no decrease/increase from OPEC or non-OPEC.

Time for you to align those demand-supply numbers with your own 2019 macro expectations.

After 2015-2016 Oil rout, many oil producers managed to reduce their production break even. According to JP Morgan estimates, the break-even oil price for BP is $46 a barrel, for Total it’s $55, for Shell $58, for Equinor $48, and for Eni $59.

40-60 is therefore a very important range for the Oil Industry. Any new oil drilling project takes between 3 and 18 months (deep offshore) before going on-line. The price stabilization we saw from mid-2016 onwards, then the rise in oil price brought new active projects down the line, i.e. from 2018. At these levels, many projects are off. $50 is a BIG level.

2014-2016 oil rout was not long ago, and many Oil Companies have stretched balance sheets. Recent moves in the stock market and in the junk bond market clearly show there is big risk below $50.

The same could be said on a country level like Saudi Arabia or Russia for example.

I hope it helps,

Gregoire

Sub Section Title Here

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum.

THIS POST

LEARN ONLINE TRADING TODAY. THE PROFESSIONAL WAY.

Let us solve the problem and confusion around trading and finance management, the right way.

ACCESS FREE LECTURESUBSCRIBE

TO OUR BLOG

To receive opinions, market research, and data analysis in the Financial Markets

ABOUT

DUPONT TRADING

As a Professional Trader/Portfolio Manager/Hedge Fund Manager for almost 20 years, I know that learning how to Trade/Invest is a non-ending learning curve. This adventure is extremely exciting but needs to be ridden carefully.

In January 2018 after receiving many requests, I decided to start my own mentoring activities.

In October 2019, I launched the 4×4 Video Series to help Investors profitably manage their portfolios. By sharing my ideas/experiences and offering education through the 4×4 Video Series, I hope I can help you becoming a better investor.

Students

Testimonials

M. (Singapore)

LEARN ONLINE TRADING TODAY. THE PROFESSIONAL WAY.

Let us solve the problem and confusion around trading and finance management, the right way.

Reader Interactions