Yes, Volatility is back!

After 2 years of low volatility (cf. blog: VIX at 24 and so what?), market is now… different.

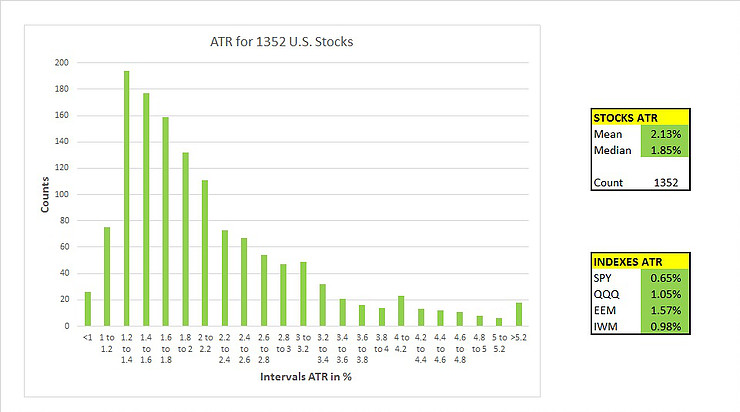

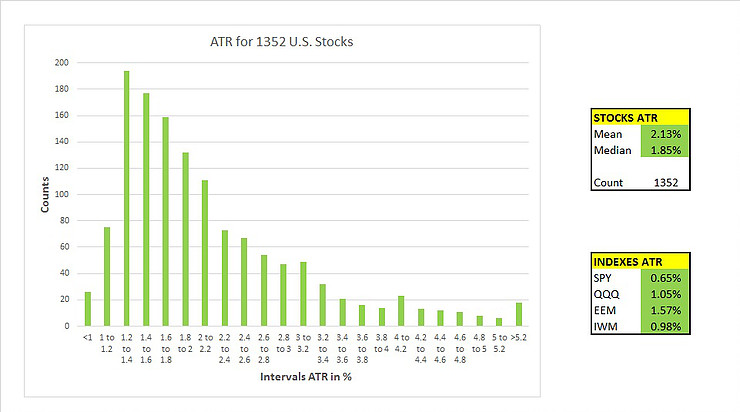

To apprehend and visualize this spike in recent volatility, the Average True Range (ATR) can be very helpful.

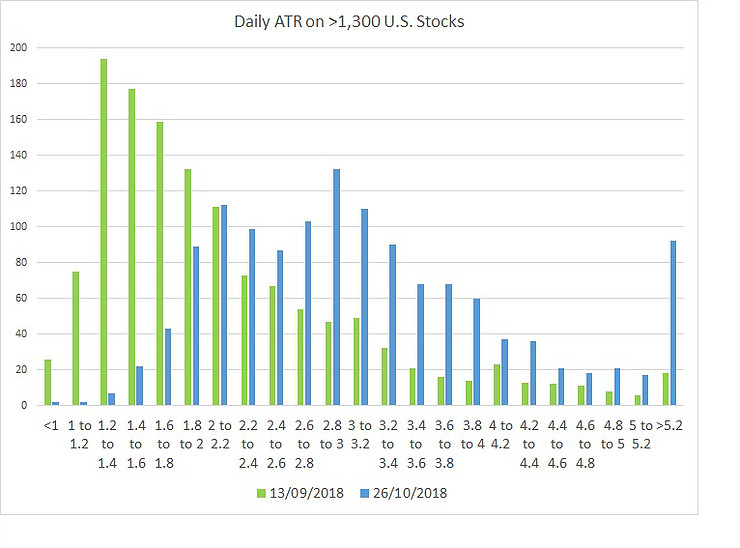

6 weeks ago, I looked at the daily ATR for more than 1,300 U.S. stocks:

https://twitter.com/GregoireDup/status/1040190100070494209

I did the same today:

Which gives the following (green 6 weeks ago vs blue today):

We moved from 2% to 3% daily ATR.

We moved from 2% to 3% daily ATR.

5% moves are x5 than 6 weeks ago.

Russell 2000 has same ATR as Emerging Markets.

Stocks can experience big moves and unlike other assets they can open with gaps.

Looking at this spike in volatility, ATR is a good tool for risk management and limiting your downside is a top priority.

In 2016-2017, we experienced very low volatility. Everything was exacerbated by low yields, passive investment, QE, share buybacks, etc.

For sure, we can put the blame on the earnings season but that would be too easy.

I hope it helps,

Gregoire

Sub Section Title Here

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum.

THIS POST

LEARN ONLINE TRADING TODAY. THE PROFESSIONAL WAY.

Let us solve the problem and confusion around trading and finance management, the right way.

ACCESS FREE LECTURESUBSCRIBE

TO OUR BLOG

To receive opinions, market research, and data analysis in the Financial Markets

ABOUT

DUPONT TRADING

As a Professional Trader/Portfolio Manager/Hedge Fund Manager for almost 20 years, I know that learning how to Trade/Invest is a non-ending learning curve. This adventure is extremely exciting but needs to be ridden carefully.

In January 2018 after receiving many requests, I decided to start my own mentoring activities.

In October 2019, I launched the 4×4 Video Series to help Investors profitably manage their portfolios. By sharing my ideas/experiences and offering education through the 4×4 Video Series, I hope I can help you becoming a better investor.

Students

Testimonials

M. (Singapore)

LEARN ONLINE TRADING TODAY. THE PROFESSIONAL WAY.

Let us solve the problem and confusion around trading and finance management, the right way.

Reader Interactions